New Tax Opportunities

Big Picture — After much deliberation, Congress recently passed the “One Big Beautiful Bill Act of 2025” (OBBB). The main result for taxpayers is that it extended the individual tax rates from the 2017 Tax Cuts and Jobs Act. There are however, a number of additional provisions that investors will want to be understand. We think for some, they may open a window for converting IRA assets to a Roth.

Roth conversions — We are giving more consideration to Roth conversions. Both traditional and Roth IRAs grow tax-fee, but distributions from traditional IRAs are taxable, which is why they are called “tax-deferred.” But distributions from Roth IRAs are not, which is why converting retirement assets to a Roth can be an opportunity.

- Standard thinking says not to convert if your future tax rate is expected to be lower than today’s. But we believe there is more to consider and as a result, more people may benefit from converting.

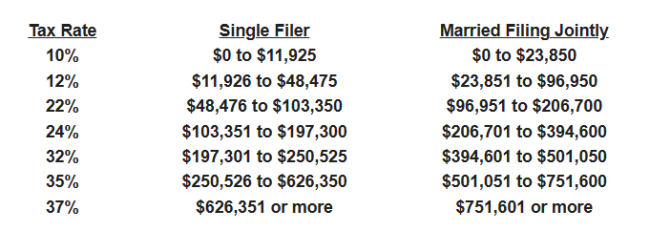

Updated Tax Brackets — To begin, the seven tax brackets will continue into 2025 but with income amounts adjusted higher:

Standard Deduction — A big change in the Tax Cuts and Jobs Act was that it substantially raised the standard deduction to a level where an estimated 90% of filers do not itemize their deductions. For 2025, the standard deduction will be increased to $15,750 and $31,500 for respectively for those single or married filing jointly.

- While the tax brackets were adjusted higher by about 2.8% to account for inflation, the standard deduction increased nearly 8%!

Reduced SALT — One of the sticking points in getting the bill passed was a provision to raise the deduction for State and Local Taxes (SALT). In 2025, taxpayers who itemize will be able to deduct $40,000, up from $10,000 previously. The new amount will be adjusted annually for inflation from 2026 to 2029 when it is set to revert back to the previous level.

Below-the-Line — Some new deductions are taken after the calculation for Adjusted Growth Income (AGI). Which means the deductions reduce the income for tax purposes, but not for some items in which use AGI to determine eligibility for other tax credits and deductions and for determining Medicare premiums.

The following below-the-line deductions are available to taxpayers whether they itemize or not:

- Tips and Overtime — Substantial deductions are available for income made from qualified tips and overtime compensation. These deductions are available from 2025 to 2028 and phase out at higher income levels.

- Senior Deduction — The new Act has created an additional $6,000 per person deduction for seniors aged 65 and older. This deduction is on top of the existing 65+ deduction. It also phases out at higher income levels and is available from 2025 to 2028.

- Donations — Taxpayers will be able to deduct charitable contributions up to $1,000 for single taxpayers and $2,000 if married filing jointly.

Haven’t been saving receipts because you don’t normally itemize? This one doesn’t start until next year!

Bottom Line — There are a number of opportunities for investors to lower their tax bills in coming years. By utilizing bracket management, investors could convert traditional retirement assets to Roths and recognizing enough income to fully utilize lower brackets.

We believe Roth conversions can be very beneficial going forward and should be considered by more investors, especially if the investors can pay the tax from funds outside the IRA. The analysis can be tricky and includes a number of variables, but it can be a beneficial exercise.